Use of biosimilars can improve competition and reduce drug costs in Canada, but their use remains very low.

Biosimilar infliximab, etanercept and insulin glargine have been listed on the formularies of all provinces; however, policies limited to patients starting a biologic for the first time (“new start policies”) have been largely ineffective at stimulating uptake of biosimilars.

Although controversial, policies that have required replacement of the reference biologic with the relevant biosimilar to maintain provincial drug coverage have resulted in large increases in biosimilar uptake since their introduction in 2019.

The biosimilars market in Canada can be strengthened through harmonization of policies, patient and prescriber education, and collaboration with manufacturers.

Biologics represent a large segment of drug spending in Canada: although they constituted just 1.5% of prescription volumes, biologics accounted for 27.3% of expenditures in 2018.1 As of 2018, the price of biologics in Canada, including spending per capita, was second only to that in the United States among the Organisation for Economic Co-operation and Development (OECD) countries.2 For example, Canada has spent more on anti–tumour necrosis factor (anti-TNF), a class of biologic drug, than on any other publicly covered medicine.3 Over the last 10 years, Canada has seen a threefold increase in spending on biologics, and this spending will continue to grow.4

With more than 1000 biologic drugs marketed in Canada and biologics now used in most clinical specialties, the need to achieve cost savings is of critical importance.5 Biosimilars — agents with similar efficacy and safety to originator drugs — offer an important avenue for cost savings.1,4,6,7 Yet, presently only 31 biosimilars are approved for use in Canada, less than half the number available in the European Union, and the use of biosimilars in Canada is relatively low.5,8

We evaluated the current state of biosimilar policies and use across Canada, highlighting 3 illustrative cases — insulin glargine, infliximab and etanercept. We briefly discuss interchangeability and indication extrapolation before making suggestions for enhancing the market through harmonization of biosimilar policies, patient and prescriber education, and manufacturer collaboration.

What is the policy context of biosimilars in Canada?

Although more than 30 biosimilars have been approved in Canada, uptake has been much lower than that of conventional generics.1,9 The Canadian policy framework for some of the earliest available biosimilars (i.e., infliximab, etanercept and insulin glargine) provides important insight into the foundation of the marketplace for these products.

Biosimilar infliximab and etanercept

The first iteration of the anti-TNF agent infliximab entered the Canadian market in 2001; in 2014, the earliest approved biosimilar infliximab (Inflectra) was marketed.5 By September 2015, the Canadian Agency for Drugs and Technologies in Health (CADTH)’s Common Drug Review published a review endorsing Inflectra for listing with similar criteria to the innovator.10 Shortly thereafter, British Columbia and Ontario listed biosimilar infliximab on their formularies for those who were starting infliximab for the first time (“new start policies”; Table 1).

Formulary list date and dates of mandatory biosimilar switching policies (if applicable) for biosimilar insulin glargine, infliximab and etanercept for the included provinces

Another anti-TNF drug (etanercept) had 2 biosimilar products approved in 2016 (Brenzys) and 2017 (Erelzi) .5 As with infliximab, CADTH’s report endorsed Erelzi for patients in whom etanercept was considered a necessary therapy under similar reimbursement criteria to the originator.10 Under new start policies, biosimilar etanercept was incorporated into provincial formularies beginning in July 2017 with BC and Prince Edward Island. It was not until 2019 that Canadian provinces began implementing policies that required patients receiving treatment to switch to the biosimilar to maintain public drug coverage.

Biosimilar insulin glargine

Long-acting insulin glargine was first approved in 2002; in 2015, a single biosimilar was authorized for sale.5 In the same year, biosimilar insulin glargine was endorsed by the Common Drug Review and was included on all provincial formularies 2 years later (Table 1).10 As with biosimilar infliximab and etanercept, provincially mandated switching was not introduced until 2019.

How has uptake varied across provinces?

At present, all provinces have listed biosimilar insulin glargine, infliximab and etanercept on their formularies. Policies that require replacement of the reference biologic with the biosimilar to maintain coverage have been announced in 5 provinces, although only BC and Alberta had begun implementation as of December 2020 (Table 1). Several other provinces and some private insurers have implemented new start policies. To explore biosimilar uptake, we used national data from the IQVIA Canadian Drugstore and Hospital Purchases Audit for all provinces except Newfoundland and Labrador from 2017 to the end of 2020.

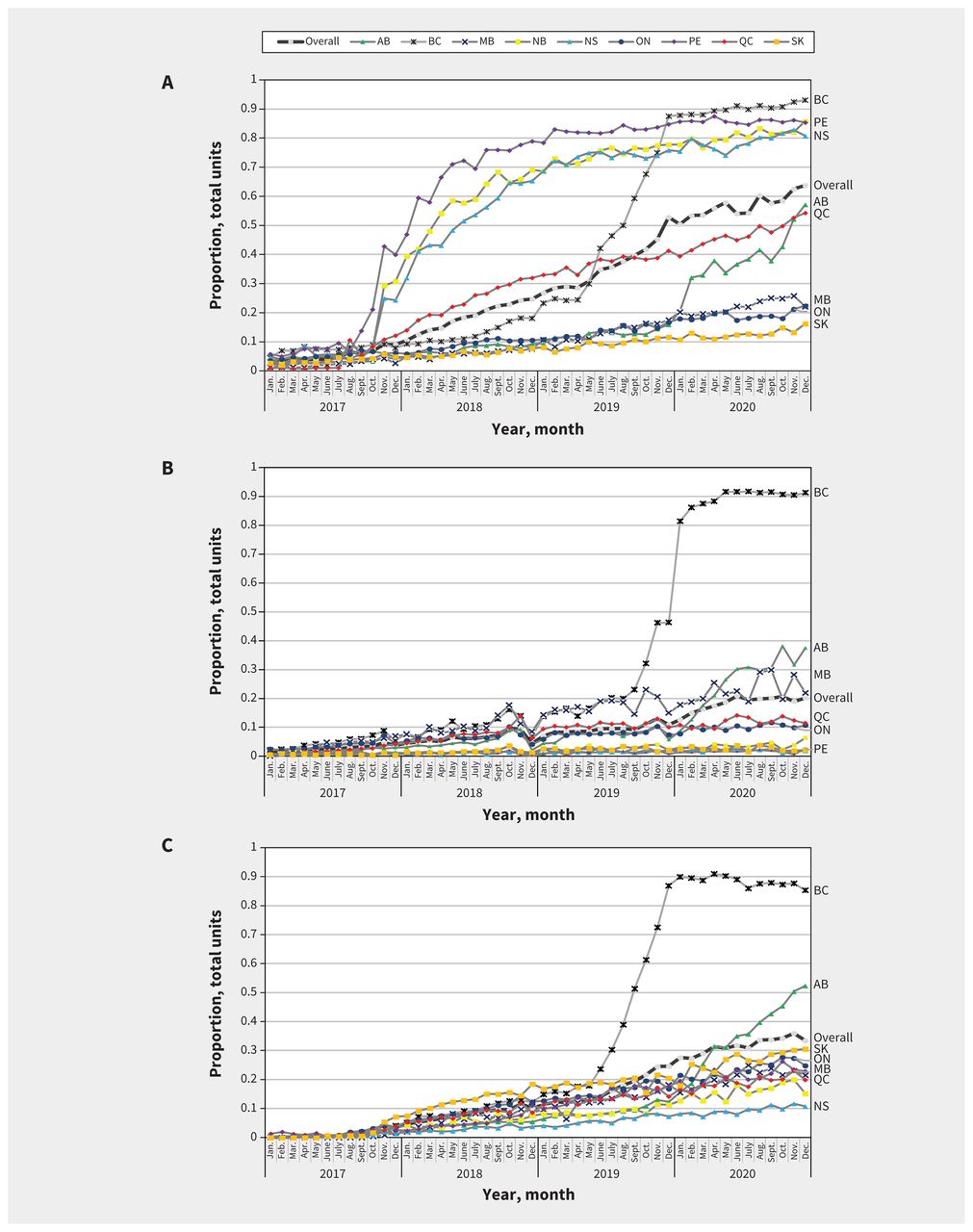

Biosimilar uptake has increased over time, albeit with substantial variation between biosimilars and across jurisdictions (Figure 1). This observed heterogeneity results in part from the piecemeal nature of Canadian drug coverage. After listing, uptake may be influenced by the availability of alternatives, and its status as a full or restricted benefit.

The proportion of total units of (A) insulin glargine, (B) infliximab and (C) etanercept biosimilar purchased from 2017 to the end of 2020 in drug stores in Alberta (AB), British Columbia (BC), Manitoba (MB), New Brunswick (NB), Nova Scotia (NS), Ontario (ON), Prince Edward Island (PE), Quebec (QC) and Saskatchewan (SK), and overall using data from the IQVIA Canadian Drugstore and Hospital Purchases Audit.

Perhaps the most dramatic example of how policy can influence uptake of biosimilars is in BC. From May to November 2019, patients receiving insulin glargine or infliximab and etanercept for certain inflammatory conditions were required to switch to the relevant biosimilar to maintain provincial drug coverage. By the end of the phase-in period, uptake of the relevant biosimilars was about 90%. In December 2019, Alberta began implementing a comparable switching policy. The early impacts of this new policy are already discernible for biosimilar insulin glargine, infliximab and etanercept. In contrast, provinces such as Manitoba, Ontario and Saskatchewan, which listed biosimilar infliximab and etanercept only under new start policies, did not see pronounced increases in uptake (Table 1 and Figure 1).

Sales of insulin glargine provide further evidence that simply adding biosimilars to provincial formularies does not ensure market penetration. For example, New Brunswick, Nova Scotia and PEI added insulin glargine as a full benefit in the fall of 2017, and, at the same time, they added a requirement for special authorization to access the originator drug. The result was a marked increase in purchases of biosimilar insulin glargine in drug stores. In contrast, Saskatchewan and Ontario introduced biosimilar insulin glargine as a full benefit around the same time without restricting access to the originator. As shown in Figure 1, there was no discernable increase in biosimilar uptake in those provinces.

What about interchangeability and indication extrapolation?

In Canada, after a generic drug receives market approval, it is automatically considered interchangeable with the reference product. This is important, as deeming a drug interchangeable means that a pharmacist can dispense the generic in place of the brand without prescriber involvement, unless the prescriber has indicated no substitutions.7 In addition, payers can mandate that the generic be dispensed in place of the brand name drug or the patient must pay the difference in price between them. Substituting a generic for the brand at the level of the pharmacy provides a mechanism by which generic uptake and market share are enhanced. Generic drugs are well received in Canada: with an overall generics market share of 76% in 2018, it is ranked third among the OECD countries in terms of uptake.9

Unlike generics, biosimilars are not deemed interchangeable with the reference drug upon approval by Health Canada and, as a result, pharmacists cannot substitute a biosimilar in place of an originator without prescriber involvement. Instead, provincial and territorial governments are responsible for deciding whether to institute policies encouraging biosimilar uptake for patients who are starting biologic therapy or for those who are already receiving originator therapy.7 However, simply listing a biosimilar does not result in the uptake that would be expected for a generic, even when several formulary strategies have been used. One reason may be clinician and patient reluctance to use biosimilars owing to unease with indication extrapolation.11

Indication extrapolation — through which the decision of similarity may be applied to other indications without conducting additional clinical trials — has been a particularly charged issue for clinicians and patients.12,13 For example, among the biosimilars discussed, studies of originator etanercept and infliximab that involved patients with rheumatoid arthritis were used as evidence for further indications (e.g., Renflexis was deemed similar enough to Remicade for treatment of ankylosing spondylitis).10 Concerns around using trial data from one indication to substantiate biosimilar use in another may help explain the divergent trends in uptake seen when comparing biosimilar infliximab and etanercept with insulin glargine.

The use of switching policies — when biosimilars are not considered interchangeable or may have garnered additional indications indirectly — is controversial. A joint position statement from the Canadian Association of Gastroenterology and Crohn’s and Colitis Canada supported the use of biosimilar infliximab in treatment-naive patients but recommended against switching from treatment with originator drugs among those who were already stable.14 In contrast, the Canadian Rheumatology Association and Canadian Spondylitis Association generally support biosimilar substitution that involves informed consent and the option to switch back to the reference biologic.15,16 Physicians and patients have also raised concerns that mental health may be affected if disease remission is not maintained and that biosimilar safety and effectiveness are in doubt.13,17,18 At least 1 originator company has provided financial assistance for patients starting treatment to obtain the reference product when faced with biosimilar competition.19 It is important to emphasize that division remains, concerns regarding biosimilar switching persist, and there are real impacts on patient and provider autonomy as a result of biosimilar switching.

However, if uptake of biosimilars remains low, manufacturers may not take the risks necessary to enter the Canadian market. This could have continued deleterious effects on both cost and access to biologics in the long term. Indeed, with only half the number of biosimilars approved compared with the European Union, Canada may already be feeling these effects.

How can we improve uptake of biosimilars in Canada?

In Canada, historical uptake of biosimilars has been lackluster (at about 1.9% of the $7.7 billion biologics industry in 2018).1 To support a healthy biosimilars market, provincial and territorial policy-makers should consider implementing a united policy front, continue education and supports for patients and providers, and collaborate with manufacturers.

Harmonization of policies

At present, Canada has a biosimilars policy salad — many public (and private) plans do not list some biosimilars at all, some list them as the default medicine for new starts only and others mandate biosimilars as the compulsory agent of choice. Provinces and territories should aim for consistency in listing and reimbursement. Policies requiring new users to start a biosimilar version do not appear to have been effective at increasing use on the national scale. Mandated switching has shown the greatest change in uptake; however, any policy that requires switching for those patients already receiving established therapy should be balanced with provider and patient education and support, as well as access to the reference drug when medically justified.

Patient and provider support

Warranted concerns around biosimilar safety and effectiveness persist among patients and providers. A systematic review of the literature available on health care providers’ beliefs found that, in general, clinicians were reluctant to prescribe biosimilars owing to safety and efficacy concerns, and concerns about indication extrapolation.14 Included studies in this review suggested a lack of knowledge of biosimilars and concluded that biosimilar prescribing may be positively affected by time and experience with these drugs. More recent evidence from a payer–provider focus group similarly proposed greater biosimilar education as a means to increase biosimilar use.20 Patient support programs for certain biologic therapies — including patient education, home delivery and nursing services — typically paid for by manufacturers also contribute to the total value of biologic therapies.5

Participation from manufacturers

With almost half the number of biosimilars approved compared with the European Union, improving uptake in Canada may incentivize additional manufacturers to undertake the risks involved in entering the market. In turn, increased competition in the biosimilars space should result theoretically in enhanced bargaining power for public and private payers and lower prices. However, the focus should not be solely on direct cost because value-added services, such as nursing services and other patient supports, are important aspects of the total value of biologic therapies.6

Conclusion

Market entry alone is not sufficient to ensure high levels of biosimilar use. The results of new start policies appear lackluster, while mandated switching has resulted in large increases in biosimilar uptake. However, many switching policies were introduced after the period we used for our analysis, and the long-term impacts of these policies remains unknown. Salient concerns among patients and providers persist, and policy-makers should proceed with caution as further evaluation is necessary. With promises of enhanced accessibility, competition and cost savings, now is the time to overcome biosimilars’ failure to launch.

Footnotes

Competing interests: Michael Law has received consultant fees from Health Canada, the Hospital Employees’ Union and the Conference Board of Canada. He has provided expert witness testimony for the Attorney General of Canada and the Federation of Post-Secondary Educators. Mina Tadrous has received consultant fees from the Canadian Agency for Drugs and Technologies in Health and Green Shield Canada. Tara Gomes is a member of the Drugs and Therapeutics Committee for Indigenous Services Canada. No other competing were declared.

This article has been peer reviewed.

Contributors: Mina Tadrous acquired the data from IQVIA. Alison McClean drafted the work. All of the authors made substantial contributions to the conception and design of the work, including revision for critically important intellectual content; gave final approval of the version to be published; and agreed to be accountable for all aspects of the work.

Funding: This research was funded by the Canadian Institutes of Health Research (CIHR) through a project grant (451221) and a 2020 Canadian Initiative for Outcomes in Rheumatology cAre (CIORA) research grant (2020-001). Micheal Law has received salary support through a Canada Research Chair in Access to Medicines. Tara Gomes has received salary support through a Canada Research Chair in Drug Policy Research and Evaluation and a grant from the Ontario Ministry of Health. Mark Harrison has received salary support through a Michael Smith Foundation for Health Research Scholar Award (16813). Mina Tadrous has received grants from the Ontario Ministry of Health and CIHR. Alison McClean has received support from the Canada Graduate Scholarships – Master’s Program. IQVIA provided data as an in-kind contribution. The statements, findings, conclusions, views and opinions expressed in this report are based in part on data obtained under licence from IQVIA Solutions Canada Inc. concerning the following information service(s): Canadian Drugstore Hospital Purchase Audit, January 2001 to December 2020. All rights reserved.

Disclaimer: The statements, findings, conclusions, views and opinions expressed herein are not necessarily those of IQVIA Inc. or any of its affiliated or subsidiary entities. The funders had no role in study design, data collection, analysis, interpretation or decision to publish.

This is an Open Access article distributed in accordance with the terms of the Creative Commons Attribution (CC BY-NC-ND 4.0) licence, which permits use, distribution and reproduction in any medium, provided that the original publication is properly cited, the use is noncommercial (i.e., research or educational use), and no modifications or adaptations are made. See: https://creativecommons.org/licenses/by-nc-nd/4.0/.

In this issue

{kind=link}

Article extras

Article tools

Jump to section

Related Articles

Cited By...

- No citing articles found.

Similar Articles

Collections